The times, they are a-changin. Last year we saw buyers sweetening their offers with everything from thousands of dollars over asking to waiving inspections. Now we are beginning to see some sellers considering incentives to attract buyers.

It’s still a seller’s market in terms of inventory, but rising interest rates have made buyers more cautious so offering incentives can go a long way toward easing some of their fear.

A 3-2-1 BUYDOWN. With higher interest rates playing a big role in buyer hesitancy, sellers can consider offering some version of a 3-2-1 buydown which actually lowers the interest rate the buyer pays for the first three years. (3% the first year, 2% the second, 1% the third, before reverting to the original rate). How? The seller pays the upfront costs at closing, called a buydown fee. While the number of points a lender charges for a buydown varies, the cost is usually equivalent to the amount the buyer saves in interest over the period of the buydown. This has been a more common practice among builders in the past and in some markets, even buyers who have cash up front might pay their own buydown points if they plan on staying in the house for a long period of time. However, in the current market, it’s more likely that buyers would be looking to sellers to facilitate a sale by offering some version of this deal (could be a 2-1, for example). Of course, buyers need to be certain that they’ll be able to pay the higher interest rate once it reverts back to it and in most cases, they’ll need to qualify for the loan at the higher rate. However, if interest rates start to decline after three years, they could consider refinancing at a lower rate. One caveat is that there could be a limit on how much “interested parties” such as the seller can contribute to a transaction so all this needs to be explored with a lender before promises are made.

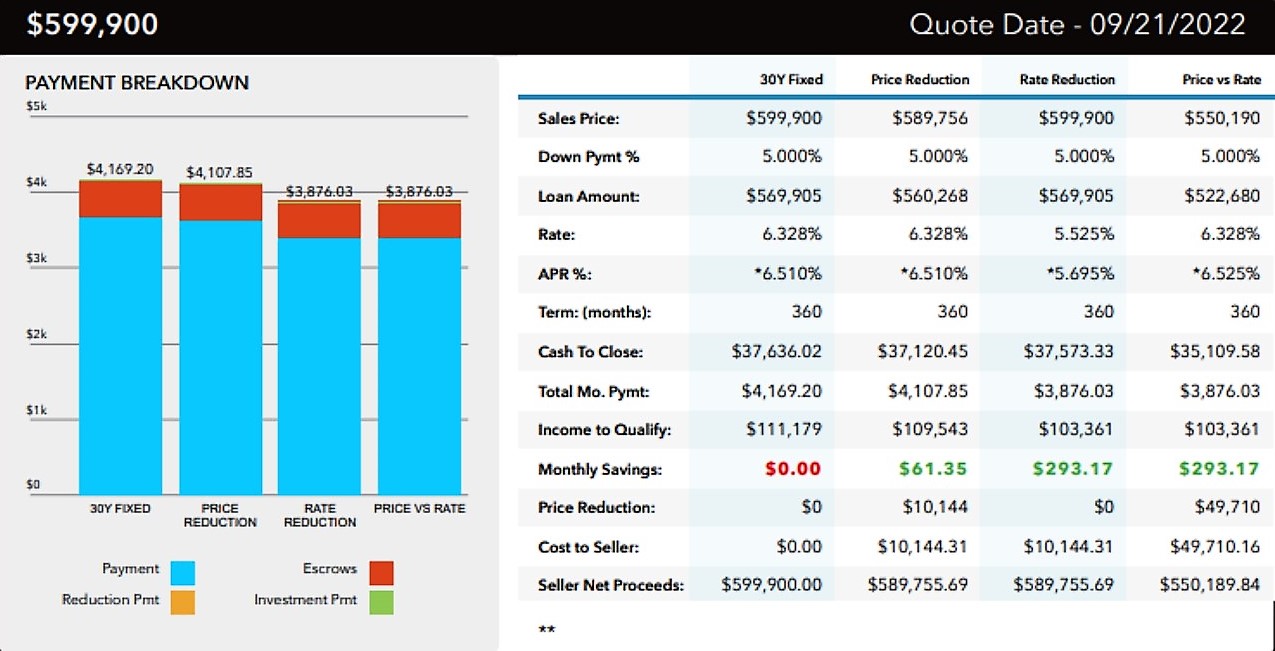

PRICE REDUCTION. This seems like an easier pill to swallow for some sellers; however, in the chart provided below you can see that a buydown explained above, in most cases doesn’t cost the seller anymore and benefits the buyer much more.

CLOSING COST CREDIT. Some buyers, especially first-timers, are often surprised to find that come closing, they will have to come up with anywhere from 3 to 6 percent of the loan amount to cover closing costs ranging from loan fees to title insurance. Sellers can offer to pay a credit to help defray these costs to the buyer.

HOME WARRANTY. Sellers can help put their buyers’ minds at ease by purchasing a home warranty at closing. Not only does it create an atmosphere of goodwill, but it also protects the seller from complaints should anything break down or go wrong after closing.

HOA DUES CREDIT. For homes in a homeowner’s association, the fees charged for maintenance can sometimes become an additional monthly expense that buyers are reluctant to take on with higher interest rates. Offering to pay the association fees for the next six to twelve months can remove a potential obstacle to closing a sale. As with the 3-2-1- buydown, sellers need to make sure they are staying within the limits of credits they are allowed to offer by the lender.

Whether you are looking to sell or looking to buy in Lake Oswego, let me put my 30+ years experience as a top Lake Oswego Realtor to work for you! Give me a call at 503.939.9801 or email me at kevin.costello@cascadehassonsir.com. Let’s find out the right strategy to help you make your next move!